Featured Article

Implementation

The Growing Fraud Landscape in Banking: A Call to Action

The banking industry faces a relentless onslaught of fraud, with staggering financial losses. The American Bankers Association (ABA) reported approximately $28.6 billion in annual fraud losses across US banks in 2023. A particularly concerning trend is the surge in account takeover (ATO) fraud, which has spiked by 72%, fueled by vulnerabilities in voice channels. Social engineering attacks targeting call centers further exacerbate the problem. To combat this evolving threat landscape, banks must implement robust, real-time fraud prevention mechanisms within their voice AI systems. These systems must be effective without introducing unnecessary friction for legitimate customers.

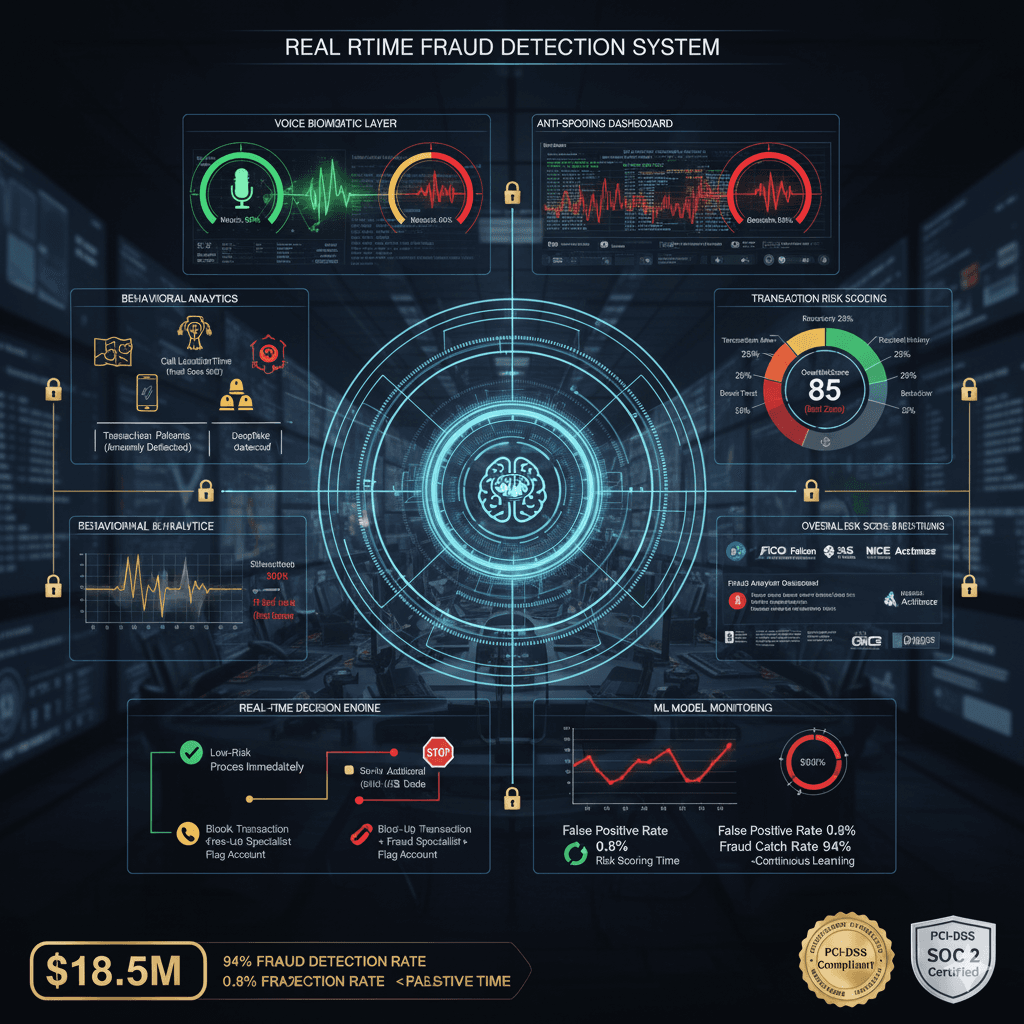

A Multi-Layered Approach to Voice AI Fraud Detection

A comprehensive fraud detection strategy for voice AI banking systems requires a multi-layered approach, incorporating several key components:

Authentication Layer: This is the first line of defense, verifying customer identity before allowing access to sensitive actions.

Behavioral Analytics: This layer analyzes customer behavior patterns to identify anomalies.

Transaction Risk Scoring: This layer calculates a real-time risk score for each transaction based on various factors.

Anomaly Detection with Machine Learning: This layer uses machine learning models to detect unusual patterns indicative of fraud.

1. Authentication Layer: Verifying Customer Identity

This layer is critical for ensuring that the person interacting with the voice AI system is indeed the legitimate account holder. Key technologies include:

Voice Biometrics: Employing voiceprint technology to match the caller's voice against an enrolled voiceprint. Advanced systems boast accuracy rates of 99.7% and can detect recording playback and synthetic voice attempts through liveness testing.

Knowledge-Based Authentication (KBA): Utilizing security questions like account numbers, the last four digits of the Social Security number, or recent transaction details.

Out-of-Band Verification: For high-risk transactions, sending an SMS code to the registered phone number for verification.

2. Behavioral Analytics: Understanding Customer Patterns

By analyzing typical customer behavior, you can detect anomalies that suggest fraudulent activity. This includes:

Device Fingerprinting: Recognizing trusted devices. A known device with an established history lowers risk, while a new or unknown device raises suspicion.

Call Pattern Analysis: Analyzing when and where a customer typically calls from. For example, a call at 2 AM from a different state when the customer normally calls during weekday mornings from their home area code should trigger an alert.

Transaction Pattern Analysis: Understanding the customer's typical transaction behavior. An attempt to transfer $5,000 to a new international account when the customer usually transfers $200-$500 to known payees is a red flag.

3. Transaction Risk Scoring: Real-Time Assessment

This component assigns a risk score to each transaction in real-time based on multiple factors:

Amount Risk: Transactions exceeding 3x the typical amount are scored higher.

Recipient Risk: Internal transfers to the customer's own account are low risk, new external payees are medium risk, and international wires are high risk.

Timing Risk: Transactions occurring at unusual times of day or week.

Location Risk: Calls originating from known locations are lower risk than those from VPNs or spoofed caller IDs.

Velocity Risk: Multiple transactions occurring within a short timeframe.

4. Anomaly Detection with Machine Learning: Identifying Outliers

Machine learning (ML) models trained on vast datasets of legitimate transactions can identify statistical outliers and suspicious patterns:

Machine learning models trained on millions of legitimate transactions identifying statistical outliers

Clustering algorithms grouping similar fraud patterns

Supervised learning on confirmed fraud cases improving detection

Fraud Detection Implementation Process: A Phased Approach

Implementing a fraud detection system requires a structured, phased approach:

Phase 1: Data Collection (2-3 weeks): Gather and prepare the necessary data.

Phase 2: Model Development (4-6 weeks): Build and train the fraud detection models.

Phase 3: Integration (3-4 weeks): Integrate the fraud detection system with existing banking infrastructure.

Phase 4: Testing (2-3 weeks): Rigorously test the system to ensure its effectiveness.

Phase 5: Deployment (2 weeks): Roll out the system in a controlled manner.

Phase 1: Data Collection

This phase is crucial for gathering the data necessary to train and validate your fraud detection models. This includes:

Integrating with core banking transaction history (minimum 12 months for pattern establishment).

Ingesting fraud case data (confirmed fraud instances with labels).

Collecting customer demographic and account data.

Establishing a data warehouse for fraud analytics.

Phase 2: Model Development

This involves analyzing historical fraud patterns, developing a risk scoring model, training machine learning models, and establishing risk thresholds.

Analyze historical fraud patterns identifying common indicators

Develop risk scoring model with weighted factors

Train machine learning models on historical data (70% training, 30% validation)

Establish risk thresholds (low 0-30, medium 31-70, high 71-100 based on fraud rate vs friction tradeoff)

Validate model performance (target: >90% fraud detection rate, <2% false positive rate)

Phase 3: Integration

This phase focuses on connecting the fraud detection system with existing banking systems:

Integrate voice biometric engine with enrollment and verification APIs

Connect to core banking APIs for real-time transaction data

Integrate with existing fraud systems (FICO Falcon, SAS, NICE Actimize) for unified fraud view

Build real-time scoring engine with <200ms latency requirement

Configure automated response workflows

Phase 4: Testing

Thorough testing is crucial to ensure the effectiveness of the fraud detection system:

Test with known fraud scenarios ensuring detection

Validate false positive rate with legitimate test transactions

Performance test scoring engine at call volume scale

Security test fraud detection logic

Conduct red team exercise (internal fraud attempt simulation)

Phase 5: Deployment

Roll out the system in a controlled manner to minimize disruption:

Shadow mode deployment (scoring runs but doesn't block, only logs for validation)

Gradual enforcement starting with highest-risk transactions (wires >$10K)

Full enforcement across all transaction types

Continuous monitoring and tuning

Specific Fraud Scenarios and Detection Techniques

Here are examples of specific fraud scenarios and how a multi-layered fraud detection system can be used to detect them.

1. Account Takeover (ATO)

Fraud: An attacker calls pretending to be the customer with stolen PII attempting password reset/transfer.

Detection: Voice biometric mismatch + unusual request pattern + unknown device.

Response: Block authentication, transfer to fraud specialist with context "possible account takeover", flag account for review.

2. Social Engineering

Fraud: An attacker manipulates a legitimate customer into authorizing a fraudulent transfer via voice AI.

Detection: Sentiment analysis detecting customer confusion/uncertainty, unusual transaction, high amount.

Response: Step-up verification, agent transfer for complex transaction counseling.

3. Synthetic Identity Fraud

Fraud: An attacker creates a fake identity with real + fake info attempting account opening.

Detection: Identity verification failure, behavioral anomalies, biometric enrollment impossible.

Response: Decline account opening, flag for fraud investigation, report to FinCEN if required.

4. Payment Fraud

Fraud: A fraudster attempts unauthorized bill payments or external transfers.

Detection: New payee never used before, amount 5x typical payment, velocity check, location anomaly.

Response: Medium-risk score triggers SMS verification, require voice biometric confirmation, limit daily payment amount pending verification.

Fraud Detection Rules Examples

Example of rules and logic.

Rule 1 (High-Risk Wire Transfer): IF transaction_type = "wire" AND amount > $10,000 AND recipient_country NOT IN ["USA", "Canada"] AND customer_wire_history_count < 3 THEN risk_score += 40, require manager approval

Rule 2 (Account Takeover Pattern): IF voice_biometric_confidence < 85% AND password_reset_requested = TRUE AND caller_id_location != customer_state THEN risk_score = 95, block authentication, alert fraud team

Rule 3 (Velocity Fraud): IF transaction_count_last_hour > 5 AND total_amount_last_hour > $2,000 AND customer_monthly_average_transactions < 15 THEN risk_score += 35, require step-up authentication

Rule 4 (Device Anomaly): IF device_fingerprint NOT IN customer_known_devices AND session_location != customer_address_city THEN risk_score += 25, require out-of-band verification

ML-Based Anomaly Detection

Examples of machine learning based anomaly detections.

Unsupervised learning (isolation forests, autoencoders) identifying transactions that don't fit customer's normal pattern without requiring labeled fraud examples

Clustering (K-means, DBSCAN) grouping similar customers and detecting outliers

Neural networks for complex pattern recognition

Continuous learning updating models weekly with new fraud patterns and false positive corrections

Fraud Response Workflows

How to response to different scoring levels.

Low Risk (0-30 score): process transaction immediately without friction

Medium Risk (31-70 score): step-up authentication required, transaction hold pending verification, agent-assist mode, reduce daily limits

High Risk (71-100 score): block transaction immediately, transfer to fraud specialist, flag account for review, automated alert to fraud operations, consider temporary account freeze

Integration with Fraud Systems

Examples of how to integrate with existing systems.

Bidirectional integration with bank's enterprise fraud platform

Real-time risk score sharing

Case management integration

Fraud alert verification

Fraud Prevention Metrics and KPIs

Example KPIs for measuring fraud prevention

Fraud detection rate

False positive rate

Fraud loss prevented

Customer friction score

Average detection time

Model accuracy

ROI

Tuning and Optimization

Keep your system efficient by weekly and montly tuning.

Weekly review of false positives identifying common patterns to whitelist

Monthly fraud pattern analysis updating detection rules

Quarterly model retraining with latest data

A/B testing risk thresholds

Feedback loop from fraud team

Regulatory Considerations

Consider these regulatory items for compliance.

Bank Secrecy Act (BSA)

FinCEN requirements

Fair Lending considerations

Customer notification requirements

Implementation Checklist

Here is a checklist before launching.

Fraud data warehouse established with 12+ months history

Risk scoring model developed and validated

Voice biometric anti-spoofing configured and tested

ML anomaly detection models trained and deployed

Real-time scoring API achieving <200ms latency

Fraud analyst dashboard and case management configured

Response workflows automated

Integration with enterprise fraud systems completed

Fraud metrics dashboard created

Security and compliance review passed

About ConversAI Labs Team

ConversAI Labs specializes in AI voice agents for customer-facing businesses.